Understanding how interest rate hikes affect US mortgages is crucial for homeowners, prospective buyers, and real estate investors. In 2026, shifts in interest rates continue to play a significant role in determining mortgage affordability and overall financial planning. This article dives deep into the mechanics of interest rate hikes, their implications on US mortgages, and practical strategies to mitigate their impact.

What Are Interest Rate Hikes?

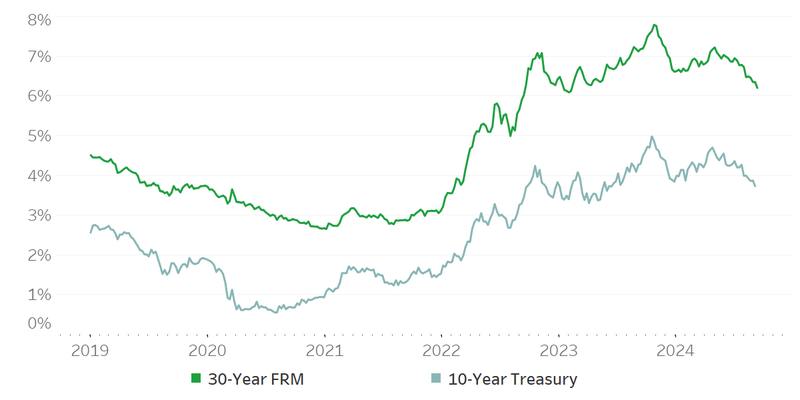

Interest rate hikes occur when the Federal Reserve raises the benchmark rates, often to curb inflation or stabilize the economy. These hikes directly affect variable-rate loans, including adjustable-rate mortgages (ARMs), and indirectly influence fixed-rate mortgages by altering lenders’ borrowing costs.

For US mortgages, even a small increase in interest rates can significantly impact monthly payments, total interest paid over the life of the loan, and home affordability.

1. Increase in Monthly Mortgage Payments

One of the most immediate effects of interest rate hikes on US mortgages is the rise in monthly payments. Higher interest rates mean that a larger portion of your payment goes toward interest rather than principal.

Example Table – Monthly Payment Impact on a $300,000 Mortgage

| Interest Rate | Monthly Payment (30-Year Fixed) | Difference |

|---|---|---|

| 5.0% | $1,610 | Base |

| 5.5% | $1,703 | +$93 |

| 6.0% | $1,799 | +$189 |

| 6.5% | $1,898 | +$288 |

As the table shows, even a 0.5% hike can increase your monthly payment by nearly $100, which accumulates significantly over time.

2. Reduced Home Affordability

Interest rate hikes reduce the amount of mortgage you can afford. For the same monthly budget, buyers can borrow less when rates rise. This affects both first-time homebuyers and those upgrading to larger properties.

Illustration Table – Borrowing Power at Different Rates

| Monthly Budget | 5% Interest | 6% Interest | 6.5% Interest |

|---|---|---|---|

| $2,000 | $372,000 | $340,000 | $320,000 |

| $2,500 | $465,000 | $425,000 | $400,000 |

| $3,000 | $558,000 | $510,000 | $480,000 |

Higher rates effectively shrink your homebuying power, potentially pushing buyers to choose smaller homes or delay purchasing.

3. Impact on Refinancing Decisions

Many homeowners consider refinancing to secure lower rates. When interest rates increase, refinancing becomes less attractive because the cost savings are smaller, or may even vanish.

For instance, if you currently have a 4.5% mortgage and rates rise to 6%, refinancing would likely increase your payment rather than reduce it. This discourages homeowners from refinancing, locking in higher interest costs over time.

4. Adjustable-Rate Mortgages Are More Sensitive

ARMs are particularly vulnerable to interest rate hikes. Unlike fixed-rate mortgages, ARMs adjust periodically based on benchmark rates. A hike can trigger an increase in your interest rate and monthly payment, sometimes dramatically.

Table – ARM Payment Example

| Initial Rate | Adjusted Rate | Monthly Payment Change |

|---|---|---|

| 4.0% | 5.5% | +$150 |

| 4.5% | 6.0% | +$175 |

| 5.0% | 6.5% | +$200 |

Homeowners with ARMs should monitor rate forecasts closely and consider refinancing to a fixed-rate mortgage if hikes are expected.

5. Total Interest Paid Over the Life of the Loan

Even a modest interest rate hike can substantially increase total interest paid. For a 30-year mortgage, a 1% increase can add tens of thousands of dollars in interest costs.

Example Table – Total Interest Paid on $300,000 30-Year Loan

| Interest Rate | Total Interest Paid | Difference |

|---|---|---|

| 5.0% | $279,767 | Base |

| 5.5% | $313,363 | +$33,596 |

| 6.0% | $347,817 | +$68,050 |

| 6.5% | $383,485 | +$103,718 |

This shows how rising rates make early planning essential for long-term financial stability.

6. Housing Market Slowdown

Interest rate hikes often lead to slower home sales. Higher mortgage costs reduce demand, leading to fewer buyers and potentially slowing home price growth. Sellers may need to adjust expectations, and the market can shift toward a buyer’s advantage.

7. Strategic Responses for Homeowners

Homeowners can take proactive measures to mitigate the impact of interest rate hikes:

- Consider Fixed-Rate Mortgages: Locking in a fixed rate protects against future hikes.

- Make Extra Payments: Reduce principal faster to minimize total interest paid.

- Refinance Strategically: Refinance when rates are favorable.

- Budget Adjustments: Adjust monthly budgets to absorb potential increases.

FAQs About Interest Rate Hikes and US Mortgages

Q1: How often does the Federal Reserve raise interest rates?

A1: The Federal Reserve reviews rates at each FOMC meeting, usually every six weeks, but changes only occur when economic conditions justify a hike.

Q2: Will higher interest rates always reduce home affordability?

A2: Yes, higher rates increase monthly payments, reducing the maximum mortgage amount a buyer can afford.

Q3: Are adjustable-rate mortgages riskier than fixed-rate?

A3: Yes, ARMs can rise with interest rate hikes, increasing payments unpredictably, while fixed-rate loans remain stable.

Q4: Can making extra payments help during rate hikes?

A4: Absolutely. Extra payments reduce the principal faster, lowering interest over time and offsetting rate increases.

Q5: Do interest rate hikes affect refinancing options?

A5: Yes, higher rates make refinancing less attractive because it may increase payments rather than reduce them.

Conclusion

Interest rate hikes significantly affect US mortgages in multiple ways—from monthly payments and borrowing capacity to refinancing options and total interest costs. Understanding these impacts empowers homeowners and buyers to plan effectively, make informed decisions, and navigate the housing market with confidence in 2026.